When discussing investing and saving, or the lack thereof, I often hear people say they’re “not good with money” or, more generally, “not good with numbers” as their reasoning for avoiding their finances.

Today, my goal is to tackle this problem.

Financial literacy is the key to unlocking financial independence, and at its core, it’s all about the numbers. Personal finance might seem daunting at first, especially if you’re uncomfortable with money or the math behind it.

Luckily, understanding and mastering a few essential math skills can make a world of difference. And don’t worry, you don’t need to dive into complex calculus or advanced mathematical theories to manage your finances effectively.

To understand the majority of personal finance, you only need to understand 3 simple concepts:

- Basic Arithmetic

- Exponents

- Compound Interest

Whether you’re budgeting, investing, or planning for the future, these fundamental math skills will empower you to take control of your financial life.

Basic Arithmetic

Basic arithmetic is the cornerstone of all mathematics. It includes addition, subtraction, multiplication, and division. Mastering these operations enables you to calculate your net worth, track your expenses, and manage various financial calculations over time. With a solid grasp of basic arithmetic, you can easily handle tasks such as budgeting, tracking spending, and determining financial goals.

Example:

Let’s say you’re a recent college graduate creating a monthly income and expense sheet, and one of the expenses you want to calculate is you’re weekly and monthly contributions to your Roth IRA. Addition allows you to sum up all your monthly income, while subtraction helps you track your expenditures—such as student loan payments, food, gas, and electricity. Multiplication and division will allow you to determine how much you will contribute to your Roth IRA weekly and monthly.

Let’s break down how we will calculate our weekly/monthly contribution:

1. You know that the annual contribution for a Roth IRA is $7,000

2. Calculate the weekly contribution by dividing $7,000 by 52

3. Calculate the monthly contribution by multiplying $134.46 by the average number of weeks in a month (4.3):

With this straightforward math, you can create an expense and income sheet that aligns with your financial goals.

Now we can create our monthly expense report:

| Item | Cost |

| Monthly Income | + $5,000.00 |

| Rent | – $1,600.00 |

| Utilities | – $450.00 |

| Car Payment | – $500.00 |

| Groceries | – $450.00 |

| Student Loans | – $500.00 |

| Roth IRA Contribution | – $578.82 |

| Remainder | $921.18 |

With a remainder of $921.18, you’re in good shape. This surplus can be used to increase savings, make additional investments, spend a little on fun, or donate to charity.

Now that we have explored basic arithmetic, let’s kick it up a notch and move to Exponents.

Exponents

Exponents might seem complex on the surface, but they are not too complicated once you get the hang of them. Exponents play a crucial role in personal finance, especially when it comes to understanding growth and decay. These concepts are essential for calculating compound interest, growth rates, and future value of investments (or debts).

In simple terms, Exponents are repeated multiplication.

Examples:

Based on the way that Exponents operate, you might be able to guess that they have a large impact on calculations.

Next, we’ll dive into compound interest, where these concepts come to life in practical financial applications.

Compound Interest

Albert Einstein famously said, “Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.” Let’s explore why this is the case.

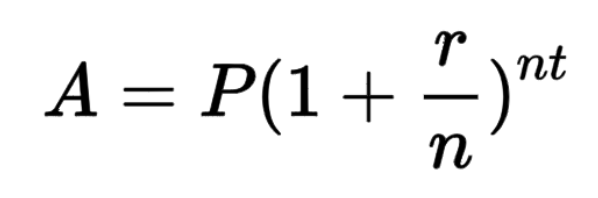

This is the equation for compound interest:

Where (A) represents the final amount, (P) represents the initial balance, (r) represents the interest rate expressed as a decimal, (n) represents the number of times interest is applied per time period, and (t) is the number of time periods.

Let’s see this in action:

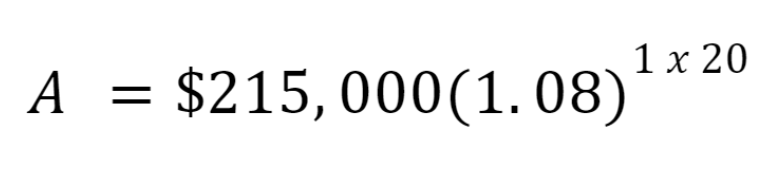

Suppose you’ve just won $215,000 and are deciding whether to spend it or invest it. You decide to invest the sum in low-cost, broad-based index funds, expecting an average annual return of 8%. You want to see how much this investment will grow over 20 years.

Variables:

- P = $215,000

- r = 8% = 0.08

- n = 1 (Annual)

- t = 20 Years

Plugging this into the equation:

Let’s break it down step by step:

1. Calculate inside the parentheses:

2. Raise 1.08 to the power of 1×20:

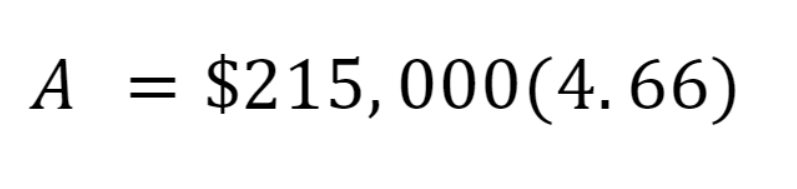

3. Multiply 4.66 by the principal $215,000:

So, after 20 years, your $215,000 investment will grow to approximately $1,001,900.00.

This illustrates the magic of compound interest. With time and consistent investment, your money can grow substantially more than the initial amount, showcasing the powerful effect of compounding.

Conclusion

Understanding the mathematics behind personal finance doesn’t require a degree in advanced calculus. The fundamental math skills displayed in this article can empower you to budget effectively, plan for the future, and make informed investment decisions. Remember, financial literacy is a journey, not a destination. Start with these basics and continue to build your knowledge over time.

As you apply these concepts to your personal finances, you’ll likely find that numbers become less intimidating and more empowering. Whether you’re creating a budget, planning for retirement, or considering an investment opportunity, these mathematical tools will serve as your compass in navigating the all too complex world of personal finance.

Don’t let a fear of numbers hold you back from achieving your financial goals. With practice and persistence, you can harness the power of mathematics to take control of your financial future. Start crunching those numbers today, and watch as your financial confidence and success grow exponentially over time. Until next time, chase your “Freedom by the Day!”